29.09.2016

Refreshed some fitting pics

Uploaded DBK, AAPL pics of volsurface fits today. Aggregated fitting pics in their own folder.

07.09.2016

New Article on Variance Strategies

"Trading realised variance using listed vanillas" recently published - see more and download

here

18.05.2016

Streamlined with list of new and updated courses. Note: software pages, which describe our main business, are in process of being updated

12.11.2015

Large numbers of new features. Too many to list

24.04.2015

Updated vols and probabilities

Quick and dirty update in

Resources as usual. Regime change confirmed for Eurostoxx skew decay.

18.12.2014

Some you win, some you lose: a short summary of our year.

PS 3.1 coming out now with important new feature added to the VolManager

Read more...

17.12.2014

Short

blog out on structural changes in volsurfaces

17.12.2014

Updated vols and probabilities

A quick approximate update of the "Resource" pages.

01.10.2014

3.0 is rolled out, after long period of beta testing. Comprehensive revamp of most features, and significant new ones added

30.04.2014

We are now providing risk services for Structured Products users.

Contact us to discuss.

30.04.2014

The big-picture talk "From delta1 to exotics and back - An apologia or an elegy for EQD?" was allegedly appreciated at conference below. Contact

Alberto if you'd like a copy

22.04.2014

We're speaking at

this London eq-der conference, and will be in Singapore 3rd-8th May (contact us if you'd like to meet)

08.09.2013

Updated resources, short

blog on implied volatility behaviour in summer and over the EM / tapering funk

12.08.2013

Updated resources (probabilities and vols): skews keeps on flattening, longer vols creep up despite spots up.

Also updated: feedback, and touched up the software pages.

25.06.2013

Updated SX5Eprobabilities

and added some pictures

19.06.2013

In

Reuters today - nothing earth shattering, just a comment on skew and market dynamics and positioning

19.06.2013

Nice to hear our volsurfaces are top in Totem submissions. Some other feedback added

here

02.04.2013

Posted two pieces in structured product blog and updated probabilities and vols

07.03.2013

Major release: version 2.0 is available

Version 2 of our software is out. Major release with many upgrades, including:

- New improved volsurface model (EQFB2), extends the global fitting region to the short maturities (~1 month)

- Multi-yieldcurve framework introduced: application to OTC pricing and structured products

- VolManager: additional fitting tools, including dividend futures and synthetics

- Data Management: all market data now viewable and editable in pop-ups, timestamps and tags added, simple tools for saving and loading from DB

01.02.2013

Improved the

glossary, and added an

italian version (thanks to one of our students at Bologna University)

30.01.2013

Interesting piece in Invesment Week

26.01.2013

Added a simple

glossary, still to be improved. Let us know what you would like to see in it.

20.01.2013

Website upgrade: probabilities

Added probabilities tables from option prices to the Resources. Formatting to be improved

05.01.2013

We have started to upgrade the website, adding more free resources, feedback etc. During this period, some of the new pages will be "under construction" - Hopefully this should create no problems, thanks for your patience.

14.12.2012

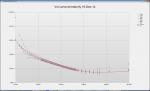

Beta testing of EQFB2 is drawing to an end

Finalised asymptotics - now fitting eurostoxx even at 10 days, and doing well even with the high OTM calls in long term SPX. (See some pictures in the download area).

We'll get round to release officially in the new year, together with all the other new features. Already available in Beta.

13.11.2012

Interview on theoptioninsider talkshow of 9-Nov is

here, from minute 14

15.10.2012

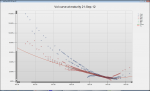

We have been working and testing on our improved volsurface model and it seems to keep on doing v well. Good fitting with only global parameters from one month expiries to several years. We'll keep on testing it, now out in beta (1.7.0). Get in touch if interested to try it. Some pictures done in august on SPX listed options.

11.10.2012

Software:1.7.0 Beta released.

Improvement to the volsurface model which extends the good fitting area to the very short maturities. Introducing the multi-yieldcurve framework, and much more.

We still consider it BETA: so let us know if you'd like to try it.

When we are happy with the final details, it will be a major release.

13.09.2012

...

added. Well, it seems funny to us...

31.08.2012

We have completed advisory work for a bank on whether to set up an equity derivative business from scratch (and how to). A separate project has seen us involved as expert witnesses.

15.05.2012

Introducing new installation and licence management system. Improvements in various functionalities.

01.05.2012

At the moment most of the interest, both sell-side and buy-side, is in volsurface modelling (e.g. illiquid underlying) and calibration of forwards and discount factors, including collateral/credit effects.

01.05.2012

Several courses delivered in March, April and May both publicly and in-house, in London, New York and Singapore

20.03.2012

More downloads for member

Added more documents for members to download, and updated existing ones

04.03.2012

Added support for different culture date formats, and more speed-ups

27.02.2012

Delivered this year's course on Equity Derivatives at

Master in Financial Math of Bologna University. Strong students, now looking for stages. Get in touch if interested.

07.02.2012

New release 1.5.0 - new tools

EQF Addin and VolManager: new tools to build yieldcurves from different sources (OIS, IRS, futures, etc), comparing them and analyising consistency vs. option-markets quotes.

Also speed-up of auto-fitting and other improvements to user-interface.

06.02.2012

The training section has been updated to reflect latest offerings - in particular, added two new courses currently being delivered both in-house and publicly

04.01.2012

Releasing 1.4.8 to fix a minor bug in a menu

23.12.2011

We are releasing 1.4.7 for

EQF Addin (minor bug fixes) and

VolManager (improvement to user interface, especially date schedules editing, referenced OTC quotes, etc)

24.11.2011

EQ DER 1: vanilla course. Running public 5,6,7 Dec in London via

LFS

08.10.2011

New versions released -Oct 2011

05.10.2011

Correlation trading course

Correlation Trading and Risk Management: public session in London on 10 and 15 October via LFS. Places might still be available.

05.10.2011

Week-long bespoke in-house training delivered to major bank in Bogota, Colombia

20.09.2011

Correlation trading course

Correlation Trading and Risk Management: public session in NY on 22 and 23 September via LFS. Places might still be available.

24.08.2011

VM is now officially out of beta testing and in production for equity indexes. Final beta testing for single stocks ongoing.

24.08.2011

Upgraded: data management, integrated datastore, Scenario Sets, quantos

19.08.2011

EQ Finance now on ICFR training catalogue

18.07.2011

EQF Addin 1.4.0 adds advanced scenarios and stress tests

Latest release of EQF Addin adds functionalities for advanced, multidimensional and multi-date scenario analysis and stress test of equity derivatives portfolios, mantaining the very simple and intuitive user interface

20.06.2011

The VolManager is now being bought even if officially still in Beta

18.04.2011

April 2011: The VolManager is now in Beta and being used against live market data. Demos available

17.04.2011

Released in EQF Addin in April 2011

17.04.2011

Variance swaps, options on variance

Released in EQF Addin in April 2011. As usual, particular care to treatment of dividend effects and others.

30.03.2011

'Correlation Trading and risk management' course

Strong demand for Correlation Trading and Risk Management. Being delivered both in-house and as a public course.

05.03.2011

Bologna University course 2011 concluded

27.01.2011

"Structured Product for Investment" course

Heavy demand recently - several sessions delivered in-house

11.01.2011

Bologna University course 2011

03.12.2010

Delivered training on "Global Exotic Derivatives" to KOFIA, in Seoul

29.10.2010

Software page updated to reflect current product line.

26.10.2010

some upgrading in training and consulting pages.

A full update of the software page is now overdue, as the software product line is growing

04.07.2010

Software tools: the generic Pricer is now ready and has been shipped to clients as an Excel addin.

04.07.2010

Correlation trading course

Public course on correlation trading and risk management will be held in London in October via another training company.

02.06.2010

New column out on Alrroya

https://english.alrroya.com/editors?auth=Alberto+Cherubini

27.05.2010

Starting another risk management project

25.05.2010

New column out on Alrroya https://english.alrroya.com/node/42791

22.05.2010

Journalist briefing at ICFR