VolSurface Dynamics

It is a hot topic for active vol traders and a research subject for quants.

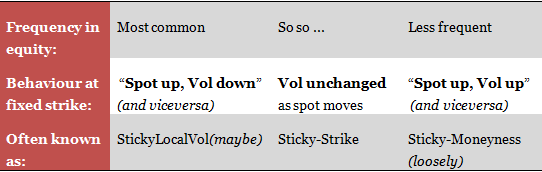

It is normally assumed that the implied volatility at a given strike and expiry will decrease when the spot price of the underlying moves up, and viceversa

Over the last 20 years~ or so this has been the most common regime, which somehow tallies with the equity skew is (nearly always) negative, i.e. the implied vol at a given maturity increases with decreasing strike.

While this is often the case, it is far from a constant behaviour.

For example, note the dynamics between march 2013 and april-may: spot up, vol up...

|

Vol ATM 3mo |

Vol ATM 2y |

Skew |

Spot |

AsOf |

|

|

SPX |

13.8% |

17.9% |

-28.0% |

1566.63 |

16-Apr-13 |

|

Eurostoxx |

17.3% |

20.7% |

-19.2% |

2814 |

21-May-13 |

|

FTSE100 |

12.1% |

15.7% |

-27.2% |

6480.4 |

02-Apr-13 |

|

|

Vol ATM 3mo |

Vol ATM 2y |

Skew |

Spot |

AsOf |

|

SPX |

12.6% |

17.3% |

-26.8% |

1549.63 |

08-Mar-13 |

|

Eurostoxx |

16.5% |

19.9% |

-19.0% |

2726.8 |

08-Mar-13 |

|

FTSE100 |

12.0% |

15.6% |

-25.2% |

6469.25 |

08-Mar-13 |

We reported (see article in Reuters) a similar period between May and June 2013: in fact over the last couple of years the "spot up, vol up" dynamic has been quite common (causing losses at some vol-trading houses and hedge funds).

This has probably been due to a decrease of demand for downside protection from the buy-side, with fund managers probably trusting the "Bernanke put", combined with a structural long skew position on the sell-side (driven by the issuance of structured products).

This new "regime" has persisted through 2014, with many cases of "spot up/vol up" or similar "spot down, vol down", while the older normal "spot down, vol up" comes back with a vengeance in period of more serious "wobbles", e.g. Aug-13, or end 2014.

___________________________________________________________________________________________

Disclaimers: all of the above is indicative and approximate, not to be used for investment purposes, should not be taken as solicitation to trade, etc